Everything about the world we live in at the moment is new (and a bit weird). COVID-19 has had far reaching economic effects. More than 2 million cases have been confirmed worldwide, including over 650,000 cases in the United States. Governments have directed people to stay at home, effectively shutting down the global economy.

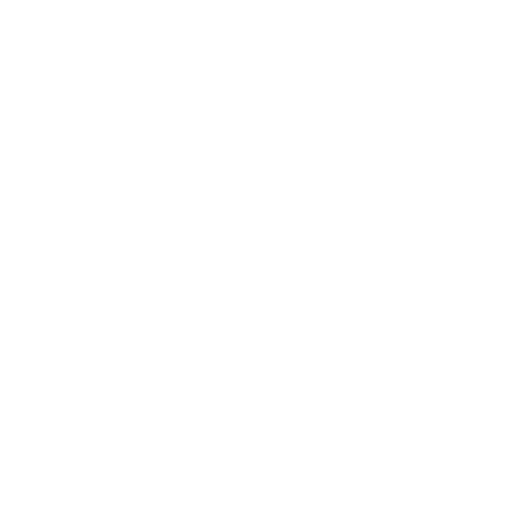

The US is the world’s largest economy by a substantial margin. An economy’s size is most often measured by the term Gross Domestic Product (GDP). GDP is the market value of all final goods and services from a nation in a given year. The United States tops the chart below with a GDP of over $20 trillion, notably due to high average incomes and a large population.

The chart shows the largest economies in the world by GDP in 2019.

For the global and Australian economies, the deep downturn we are currently experiencing is unique. Effectively it is a recession by Government decree.

Through February & March, most nations moved to close down large components of their economies – tourism, hospitality, main street discretionary retailing etc. In addition, encouraging those that can work from home to do so has also had a material economic impact as public transport and motor vehicle usage has collapsed and the service industries supporting the high population density of a CBD during business hours saw their customer base disappear.

In America, in just 4 weeks, 22 million Americans have lost their jobs. Retail sales posted last month recorded the biggest fall on record and industrial production plummeted.

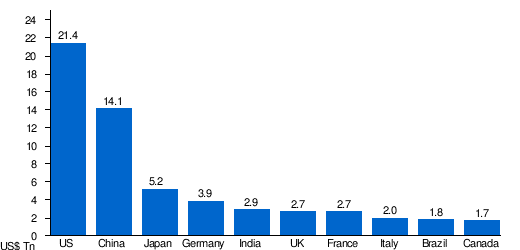

This all equates to an economic shock that will deliver the deepest recession – global & in Australia – that we have seen since the Great Depression in the 1930’s. The International Monetary Fund (IMF) are forecasting that the global economy will contract by 3% in 2020 (as shown in the chart below) as measured by GDP.

Whilst this all looks pretty ugly, the bulk of the economic pain is going to be booked in the June half, particularly the June quarter which we are in now. Many major companies will post very poor financial results, some will need to raise capital, and some, in particularly exposed industries, may not survive. The swift negative share market reaction, as best indicated by the S&P 500 (the largest 500 companies listed on the US stock exchange) which fell 33% over a 30 day period to its low on 23rd March, is a stark reflection of this fact.

However, the positive aspect of the chart is that the IMF are forecasting a significant rebound in 2021. And with a refocus on the long-term economic activity and a rebound in company earnings, this gives investors reasons for a more positive outlook heading into 2021. However, we must be prepared for continued extreme levels of volatility in the short term in response to day to day information and investor sentiment.

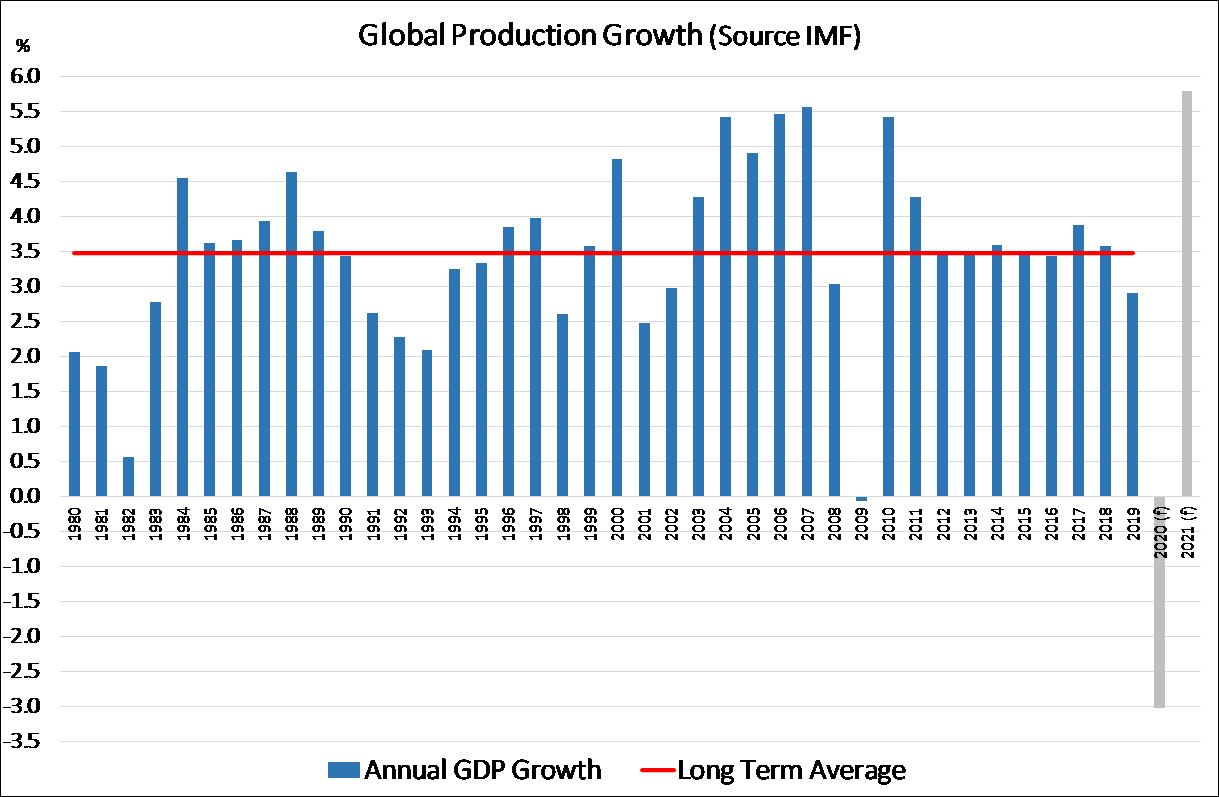

China is an interesting economic study. The most recent data suggests China is back on track. A much-watched economic indicator of manufacturing activity has rebounded strongly in March, after plummeting in February, as China returned to work. It indicates a broad stabilization of business conditions as firms reopened following widespread company shutdowns and travel restrictions in February amid the COVID-19 outbreak. The IMF have indicated that China’s Economic Growth is still likely to be positive this year, although this number is significantly lower than it has been in the past.

China’s manufacturing activity (2011 – 2020)

The graph shows China’s manufacturing activity (as depicted by the Purchasing Managers Index or PMI) data over the last decade. With reference to the horizontal line, a measurement of 50 indicates no change to activity, a figure below 50 represents a contractionary environment.

So, if the figures can be believed, a sharp turnaround in China is underway. The global economy will take a lot longer.

In Australia’s case, the economy is forecast to contract by approximately 6% in the current June quarter alone. While it is still too early to be definitive, this could be as bad as it gets. If the government decrees, which have caused the recession, are eased over coming months, there is a good chance that economic activity will recover through the December half (as is implied in the IMF’s forecast for 2020).

Governments around the world – including Australia – have unleashed unprecedented fiscal support. In combination with the similarly generous actions of central banks, the preconditions are in place for a strong rebound. All these policy measures will not prevent a recession, but they will assist in the recovery phase – particularly via supporting the financial position of households through a period of escalating unemployment.

It will probably take 6-12 months for all the various restrictions that have closed the global economy to be lifted.

The risks to this forecast are the negative implications of the virus re-emerging (second wave), and that the recovery will not be compromised as the massive support initiatives from Central Banks and governments run off.

Assisted by all the stimulus measures announced over recent weeks and the containment in the spread of the virus in most developed economies, financial markets are assuming that the outlook will improve from mid-year and that a level of normality will return in 2021.

Please feel free to contact your Paradigm Group advisor should you wish to discuss any issues in relation to your specific circumstances.

Patrick Nalty & James Mirams, Paradigm Group – Directors