It has been a tumultuous month for the world economy and financial markets as a result of the onslaught of the coronavirus.

At the end of February, the global economy was in good shape, as was the Australian economy, and Australian companies post the reporting season, in general, were well placed.

Within a few weeks, this changed with incredible swiftness and severity.

Managing a portfolio of Australian shares is very challenging in such a fast-moving environment with such uncertainty. At the end of the day, investors who own Australian shares are long term investors, and are aware of the volatility that can occur; however, some companies and sectors can be impacted more severely or for longer when conditions deteriorate. This factor is the reason why portfolio changes are necessary, and it is through this activity that value can be added.

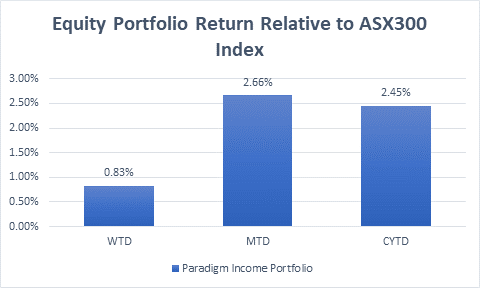

The chart below, updated to 26th March, indicates the positive performance of the Australian Share Income portfolio when compared to its benchmark (the ASX 300 – an index of the largest 300 Australian companies). The portfolio has outperformed the index strongly over the last week, the month of March to date, and the calendar year to date.

Over the last several weeks, the Australian Share Income portfolio has been active in adjusting a number of holdings, to reduce exposure to companies or sectors that are affected more severely in the current conditions, whilst seeking value in other opportunities.

For your interest, we have set out below some of the recent material changes that have been made and the reasons.

SALES

National Australia Bank (NAB)

NAB had performed strongly on the prospect of improved operational performance under the new CEO, Ross McEwan. However, with a changing environment, NAB will face challenges driven by an inflating cost base with the potential for further remediation charges post the Royal Commission. Moreover, the broader banking sector is facing the dual headwinds of a weak economy as well low rates with subsequent pressure on profit margins, as such the holding in NAB was sold.

Suncorp (SUN)

In response to economic factors, the Reserve Bank of Australia slashed interest rates to a record low. Lower interest rates are set to impact returns in the insurance and banking business, and as a result SUN was sold.

South 32 (S32)

S32 is a diversified mining company operating across a range of commodities and jurisdictions. However, this comes with complexity when countries close their borders and transportation becomes an issue. During the current challenges globally, there is a focus on increasing the exposure to commodities that have performed the strongest over this period and have domestic operations. Hence, we have sold S32 in order to rotate funds to Rio Tinto, a world leading low cost iron ore producer.

ACQUISITIONS – NEW HOLDINGS AND ADDITIONS

Telstra (TLS)

The defensive nature of Telstra becomes a stand-out in an uncertain environment. It remains a market leader in all vital telecommunications segments. Whilst many companies have recently withdrawn their earnings guidance, Telstra has commented that its outlook remains within the range of its previous guidance, albeit at the bottom end of this range. This is a positive announcement in light of the current circumstances, and also indicates the dividend is likely to remain steady.

Rio Tinto (RIO)

RIO is now trading down more than 30% from its recent high. With the bulk of earnings coming from the Pilbara Iron Ore operations we see low risk of disruption and a robust outlook for demand as China moves to stimulate its economy post the coronavirus slowdown. A lower Australian Dollar provides earnings support as all shipments are based in US Dollars. With a strong balance sheet and now a sustainable yield above 7% we see opportunity to benefit from strong returns going forward.

Amcor (AMC)

Primarily exposed to non-discretionary goods, the company’s revenue line should remain resilient to global turbulence, with margin upside potential from lower input costs.

Management is very capable of maximising the current opportunities and we remain very positive on the outlook for the company. We view the current weakness as a rare opportunity to ADD to the existing holding in a well-managed Australian company with leading positions in global markets.

Please feel free to contact your Paradigm Group advisor should you wish to discuss any issues in relation to your specific circumstances.

Mike Hawkins, Paradigm Group – Investment Committee Chair