Australia

The federal Budget was handed down a month before the regular budget season, presenting tax measures to please key voter groups, a further boost to infrastructure spending, and the much-vaunted return to surplus. As expected, the underlying cash balance is forecast to return to a surplus of $7.1 billion in 2019-20, or 0.4% of GDP. The government is assuming GDP growth of 2.25% this financial year, rising to 2.75% in 2020-21 (with consumer spending forecast to grow at similar rates), but even these figures appear somewhat optimistic. GDP growth of just 0.2% was recorded in the December quarter, in line with the September quarter’s figure, leaving annualised growth at just 1.0% in the second half of 2018 compared with the 4.0% pace in the first half. With core inflation remaining below target, the shift in RBA policy bias from tightening to neutral seems totally justified.

Employment growth slowed in February with 4,600 jobs. The unemployment rate decreased 0.1 points to 4.9% while the participation rate fell 0.2 points to 65.6%.

The AIG Manufacturing Index slowed in March and appears to be holding to its downward trend, falling to 51.0. Manufacturing activity has been affected by the global slowdown as well as the downturn in housing construction, although certain sectors such as Food & Beverages and Textiles are still showing solid growth.

Australia’s balance on goods and services rose in February to a surplus of $4,801 million. Exports of metal ores and minerals added $958 million over the month but this was offset by a fall in the value of coal, coke and briquettes exports of $760 billion. On the debit side, imports of general merchandise fell by $587 million and intermediate goods improved by $443 million.

The Westpac Melbourne Institute Index of Consumer Sentiment slipped back into ‘cautiously pessimistic’ territory in March, falling to 98.8. The main economic news over the period was the December quarter national accounts, which recorded a contraction in economic growth and appears to have darkened the mood of consumers. Despite the shift in the RBA’s rhetoric, consumers still seem concerned about interest rates.

Global

The slowdown in US growth in the early months of 2019 has been confirmed by incoming data and follows a sharp downturn in the last quarter of 2018. With inflation slipping back below the Fed’s target, markets have dramatically shifted their expectations for the next interest rate move, with a cut to the funds rate firming as a possibility. March non-farm payrolls delivered a strong result with 196,000 additions, which was ahead of expectations and a relief for markets following February’s shock result. Core capital goods orders, an indicator of business investment, jumped 0.9% in January after two consecutive monthly declines before falling to -0.1% in February. Other economic data has been on the weak side, although March has seen some small signs of improvement.

The ECB sharply cut its expectations for growth from 1.7% to 1.1% for 2019 and from 1.7% to 1.6% for 2020. ECB President Draghi referred to weak data from the manufacturing sector arising from a slowdown in international demand and specific factors, including Brexit, ongoing disruption in the auto industry, and the US-China trade dispute. Inflation in the eurozone fell to 1.4% in March, but manufacturing is in its deepest downturn in almost six years, offset by greater resilience in the services sector. However, the euro area is being supported by a strong labour market and gradually rising wages.

UK Prime Minister May’s Brexit deal has been convincingly rejected by the parliament three times. If no deal is agreed to, the UK will face an exit date of 12 April. May’s plan is to negotiate with Labour leader Corbyn to craft a bipartisan deal that can pass the House of Commons and be presented to European leaders.

The news out of China has been slightly more positive over the past month, with March PMI figures improving and retail sales growth stabilising. signs of progression on trade talks with the US and evidence that stimulus measures are supporting activity have also been positive.

Commodities

Oil prices forged ahead in March as the supply outlook was curbed by a fall in OPEC output for the fourth straight month and Venezuelan production suffered from the ongoing economic and political crisis. Metals were generally softer in March, with falls in Lead, Tin, Nickel and Copper.

Australian Shares

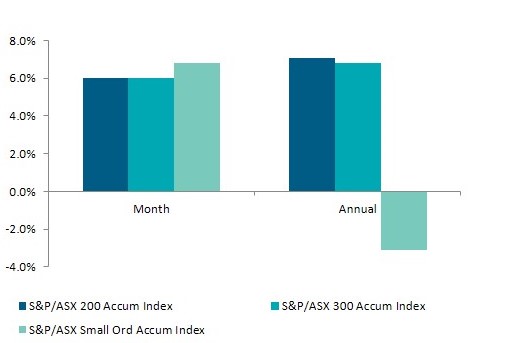

After rising 10.1% over January and February, the S&P/ASX 200 Index paused in March, returning 0.7% before regaining momentum in the first week of April.

Over the past year, the ASX has delivered a total return of 12.1%, driven predominately by the 50 largest shares, while the small cap index has returned only 5.8%.

International Shares

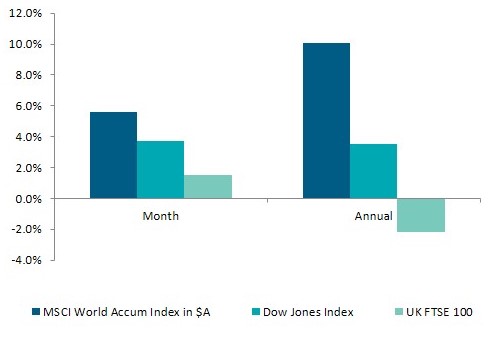

Global shares remained buoyant in March but appeared to run out of steam after rallying hard through the start of the year.

The US S&P 500 Index rose 1.9% through the month in US dollar terms, led by the IT sector.

The STOXX Europe 600 Index rose 1.7% in March. Germany’s two biggest banks, Deutsche Bank and Commerzbank finally announced that they are actively considering a merger.

China’s markets continued to rally strongly through March on the back of stimulus announcements and progress in trade talks.

Property

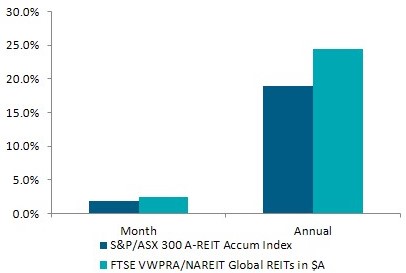

Australian listed property left other sectors in its wake in March with the S&P/ASX 200 A-REIT Index returning 6.2% with broad gains across the board. As the recovery in equities took some time out in March, the search for safe-haven assets continued, with investors attracted to the promising outlook for earnings and distributions in the A-REIT sector.

Generally, debt levels are seen as sustainable and investors have even enjoyed a rise in Net Tangible Assets in recent months, especially in industrial and office assets, although retail still faces some significant headwinds.

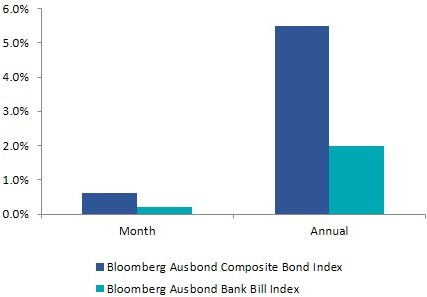

Fixed Interest

While equity markets stabilised, bond markets sounded alarms for investors as rapid falls in long-term yields resulted in an inverted yield curve (historically a signal that a recession is on the way).

In Australia the 10-year yield dropped from 2.10% to 1.77%, a decline of nearly 60 basis points since the start of 2019.

Global bonds, measured by the Bloomberg Barclays Global Aggregate Index, returned 1.7% over March in Australian dollar hedged terms, while Australian bonds returned.

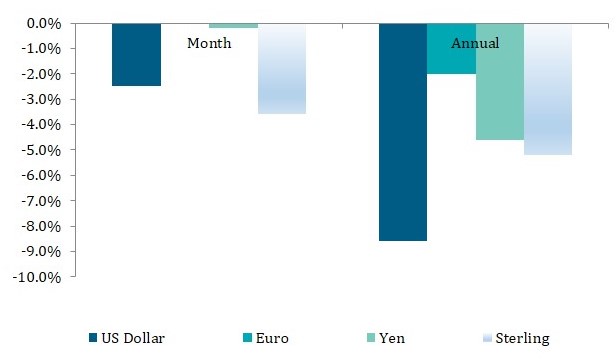

Australian Dollar

The Australian dollar was mostly flat against the US dollar in March and has held above 70 cents over the past six months, supported recently by a softer US Fed outlook, which has eased fears of a widening interest rate differential.

The Australian dollar rose against other major currencies during the month, including the British pound and the euro but was softer against the Japanese yen.

Key Investment Indices

| As at 31 March 2019 | 1 month | 3 months | 6 months | 1 yr | 5 yrs | |

| Australian Shares | % | % | % | % | % | |

| S&P/ASX 200 Accumulation Index | 0.7 | 10.9 | 1.8 | 12.1 | 7.4 | |

| S&P/ASX 300 Accumulation Index | 0.7 | 10.9 | 1.6 | 11.7 | 7.4 | |

| S&P/ASX Small Ordinaries Accumulation Index | -0.1 | 12.6 | -2.8 | 5.8 | 8.0 | |

| S&P/ASX 300 Industrials Index | 0.4 | 9.0 | -0.2 | 8.3 | 7.5 | |

| S&P/ASX 300 Resources Index | 1.9 | 18.8 | 8.8 | 26.9 | 6.6 | |

| International Shares | Value | % | % | % | % | % |

| MSCI World Accumulation Index in $A | 1.5 | 11.5 | -0.9 | 12.3 | 12.8 | |

| MSCI World Accumulation Index ($A hedged) | 1.7 | 12.6 | -2.7 | 6.5 | 9.7 | |

| MSCI Emerging Markets Index in $A | 1.0 | 8.9 | 3.6 | 0.0 | 9.3 | |

| Dow Jones Index in $US | 25,929 | 0.1 | 11.2 | -2.0 | 7.6 | 9.5 |

| S&P 500 Index in $US | 2,834 | 1.8 | 13.1 | -2.7 | 7.3 | 8.7 |

| FTSE 100 Index in £ | 7,279 | 2.9 | 8.2 | -3.1 | 3.2 | 2.0 |

| Nikkei 225 Index in ¥ | 21,206 | -0.8 | 6.0 | -12.1 | -1.2 | 7.4 |

| Deutsche Boerse Index in € | 11,526 | 0.1 | 9.2 | -5.9 | -4.7 | 3.8 |

| Hang Seng Index in HKD | 29,051 | 1.5 | 12.4 | 5.5 | -3.5 | 5.6 |

| Shanghai Shenzhen CSI 300 Index in RMB | 3,872 | 5.5 | 28.6 | 12.6 | -0.7 | 12.5 |

| Property | % | % | % | % | % | |

| S&P/ASX 200 A-REIT Accumulation Index | 6.2 | 14.8 | 12.6 | 26.2 | 14.8 | |

| S&P/ASX 300 A-REIT Accumulation Index | 6.0 | 14.4 | 12.4 | 25.9 | 14.9 | |

| FTSE EPRA/NAREIT Global REITs in $A | 3.1 | 13.3 | 9.5 | 22.9 | 12.3 | |

| Fixed Interest | % | % | % | % | % | |

| Bloomberg Ausbond Bank Bill Index | 0.2 | 0.5 | 1.0 | 2.0 | 2.1 | |

| Bloomberg Ausbond Composite Bond Index | 1.8 | 3.4 | 5.8 | 7.2 | 5.1 | |

| Barclays Global Aggregate Index ($A Hedged) | 1.7 | 2.8 | 4.5 | 4.6 | 4.8 | |

| Inflation | % | % | % | % | % | |

| Australia CPI | 0.2 | 0.4 | 1.0 | 1.8 | 1.7 | |

| Currencies (relative to $A) | Value | % | % | % | % | % |

| $US | 0.7096 | 0.0 | 0.7 | -1.8 | -7.6 | -5.2 |

| Japanese ¥ | 78.6670 | -0.5 | 1.8 | -4.2 | -3.6 | -3.8 |

| Euro € | 0.6326 | 1.4 | 2.9 | 1.6 | 1.5 | -1.2 |

| Sterling £ | 0.5445 | 1.8 | -1.5 | -1.8 | -0.7 | -0.4 |

| Chinese Yuan | -0.4 | 1.3 | 1.3 | 1.1 | 3.8 | |

| Commodities | Value | % | % | % | % | % |

| S&P Goldman Sachs Commodity Index ($US) | 1.8 | 16.0 | -10.7 | -4.2 | -7.7 | |

| Oil ($US/barrel) | 68.39 | 5.1 | 32.4 | -17.9 | -7.4 | -10.0 |

| Gold ($US/ounce) | 1,292.38 | -1.6 | 0.8 | 8.5 | -2.5 | 0.1 |

| Iron Ore ($US/tonne) | 86.37 |

Sources: Lonsec, Atchison Consulting, Colonial First State