Global share prices continue to suffer negatively from unrelenting inflationary pressures, that have been higher and more persistent than economists expected. The connectivity between inflation and the value of shares lies with the expectation over interest rates. It is feared that current inflation numbers could lead to the Federal Reserve in the US increasing interest rates much faster than previously expected.

The economic challenge is to make these adjustments to interest rates without stifling consumer demand and investor sentiment to such an extent that it drives the US economy into a recession. This is the concern of the market at this time.

As a consequence, the index of the top 500 companies in the US, the S&P 500, has dropped more than over 20% from its highs. The technology focused Nasdaq Index, weighted towards global titans including Apple, Microsoft, Amazon, Tesla and Alphabet (Google) has fallen over 30% as growth focused companies such as these depend more on a growing economy. Australian shares indices were somewhat buffeted due to the exposure to energy and resources companies, but the ASX 300, the index of Australia’s largest 300 companies, has fallen over 12% in the last 2 months, to its lowest point in 18 months.

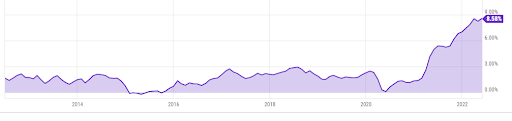

Most recent US inflation data showed that US inflation was significantly higher than even updated economic forecasts, with the US consumer price index (CPI) for May rising 8.6% from a year ago, the highest increase since December 1981. Consumer demand combined with the challenges of the drawn-out war in Ukraine affecting food and energy supply and prices, and protracted COVID lockdowns in China have continued to affect the global supply chain. Surging energy and food prices contributed to the CPI gain, rising 34.7% and 10.1% respectively over the period. The 10-year graph below shows the sudden sharp rise in CPI.

In containing inflation and inflationary expectations, all central banks can do is suppress private sector spending – the demand side of the supply/demand imbalance that has created the inflationary pressures. Supply driven price pressures, caused by product shortage or logistical challenges may persist for a time but ultimately, they too recede.

As such, the extent of central rate increases is unlikely to be determined by whether inflation hits 5% or 15%. Rates will pause/peak when evidence is in hand that private sector spending has curtailed, and the unemployment rate is poised to rise. Inflation and inflation risks have certainly intensified but it is very unlikely that the level of rates required to suppress private sector activity is any different today to what it was a year ago.

Accordingly, ramping up tightening expectations alongside actual inflation outcomes may be shown to be a gross overshoot. Understandably, markets will need to see hard evidence that private sector activity is cooling for this reflex response to be challenged. In this regard, housing activity/prices are already faltering. What we are yet to see is a capitulation in discretionary spending by households. This is highly likely to materialise over the remainder of the year.

At that point, central banks, particularly the Federal Reserve, will be in a position to pause regardless of where inflation then happens to be sitting. Both the US and Australian bond markets are currently projecting that the cash rate will hit ~4% in late 2023. As such, a pause that is well short of this expectation, would be welcomed by both bond and equity markets.

The Paradigm Investment Committee makes decisions based on long term investment themes, given the assets being managed, particularly in shares, are long term in nature. The Investment Committee recognises that short term volatility and negativity can create concern, but remains focused on long term asset allocation targets, and believes that over the long term, that component of an investor’s portfolio that is exposed to shares and share funds is broadly directed to assets that will exhibit long term growth. History shows that bouts of significant volatility occur every few years, and patience, and time, ultimately are the factors that will reward long term investors.

Fixed Interest and Alternative asset classes continue to do their job to provide some stability to the conservative component of portfolio structures.

As always, if you have any specific queries, please contact your Paradigm advisor.